The Indiana University campus relies on multiple sources of income, including tuition from undergraduate and graduate students, state appropriations, donor gifts through IU Foundation, Indirect Cost Recovery from grants and contracts, and other, smaller sources, such as clinical services or sales.

Funding Allocation

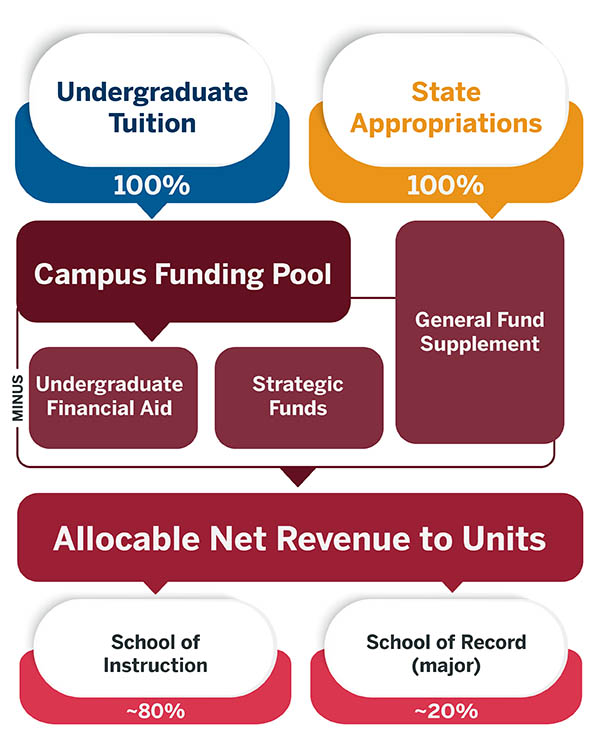

The two primary sources of income for the campus are undergraduate tuition and State Appropriations.

Academic year undergraduate tuition, both resident and non-resident tuition, will flow into a Campus Funding Pool. Before distributing the majority of the Campus Funding Pool to academic units, a proportion will be held centrally for three purposes: undergraduate campus-based financial aid, strategic initiative funds, and as needed, the General Fund Supplement.

The allocation amounts to each of these funds will be reviewed every two years by the Provost Academic Leadership Group (composed of deans, vice provosts, and other leaders) and the IUB Financial Advisory Committee with the goal of having set amounts for each biennium to aid in planning.

The primary purposes for each fund are as follows:

Undergraduate financial aid will continue to be covered by campus funds to ensure broad access to education for top students from across Indiana and beyond. Financial aid levels and the tuition discount rate will continue to be reviewed annually with a goal of lowering the discount rate through new financial aid strategies that leverage data-driven metrics.

Strategic Funding will continue to be used for strategic priorities of the Bloomington Campus, including annual Provost Fund requests and strategic investments in the 2030 IUB Strategic Plan. It will also include outcomes-based metrics designed to incentivize key priorities such as research and creative activity productivity, student success metrics, and others.

The General Fund Supplement (GFS), which includes State Appropriations, will support academic units with funding for the annual salary pool increase and common good needs to maintain excellence across a comprehensive public research university. GFS will also help units transition to the new budget model. After the first two years, amounts may change in consultation with the Provost and academic deans each biennium.

The remaining revenue (i.e., "Allocable Net Revenue to Units" in the diagram below) will be distributed to academic units, based on course enrollment (e.g., a set rate per credit hour taught). Schools of instruction will receive 80% of that rate, and the schools of record (students' major school) will receive 20% of the rate. The new split helps ensure that units receive funding for supporting the costs of instruction as well as the costs of recruiting, advising, and providing enriching programming to their majors.

Expense Allocation

Academic units help cover central campus expenses, such as student life, enrollment management, undergraduate education, the graduate school, faculty and academic affairs, and others. The Steering Committee recommended that a metrics-based formula be used that could be roughly tied to usage. Potential metrics will be modeled during the Prototype Phase and could include:

- Academic appointment FTE (includes tenure track, non-tenure track, and other full-time academic appointments)

- Staff FTE

- Student headcount or credit hours (both will be modeled during the Prototype Phase)

- Assignable square footage

- Direct expenses

The campus is continuing to collect feedback and will review alternatives that develop during campus conversations before determining the final model for allocating central expenses.